Most of the world is racing to add renewable megawatts this decade. India is playing a different game. On 6 April 2026, at 8:25 PM IST, the Prototype Fast Breeder Reactor (PFBR) at Kalpakkam achieved first criticality. It is the kind of milestone that does not move markets the next morning, but quietly changes what is possible over the next century. For VCs and operators watching the energy transition, the signal matters more than the spectacle.

India holds 1 to 2 percent of the world’s uranium but nearly 25 percent of its thorium. The PFBR is the bridge between those two numbers.

The Bhabha Blueprint

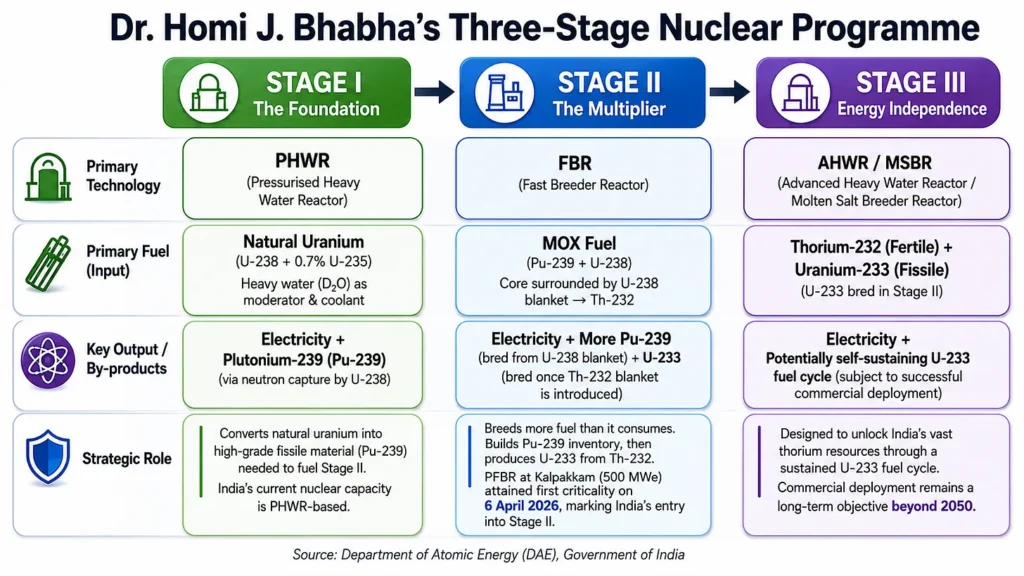

Back in the 1950s, Homi Bhabha designed a three-stage programme to turn India’s resource constraints into a long-term strategic advantage. Stage I uses scarce domestic uranium in heavy water reactors to generate plutonium. Stage II uses that plutonium in fast breeder reactors to produce more fissile material than it consumes. Stage III uses the bred material to finally unlock India’s 1.07 million tonnes of extractable thorium, concentrated in the monazite sands of Kerala, Tamil Nadu, Odisha and Andhra Pradesh. It is sequential by design. You cannot skip a stage. For seventy years, India has been patiently feeding the first stage to earn the right to run the second, as detailed below.

Source: Public Information Bureau, Bhabha Atomic Research Institute, PIB India Thorium Reserve

Why the PFBR Is the Inflection Point

The Prototype Fast Breeder Reactor is a 500 MWe, sodium-cooled, pool-type reactor designed by the Indira Gandhi Centre for Atomic Research and built by BHAVINI. It runs on uranium-plutonium mixed oxide fuel surrounded by a fertile U-238 blanket. Fast neutrons drive fission while converting the blanket into fresh Pu-239. In plain terms: it makes more fuel than it burns. Only a handful of countries operate breeders at scale, most notably Russia’s BN-800.

The project was sanctioned in 2003 with a 2010 target and a Rs 3,492 crore budget. It achieved criticality in 2026 at roughly Rs 8,181 crore. For context, China’s CFR-600 took six years, but it leaned on existing partnerships. India built PFBR end to end without foreign technology transfer on core systems. Slow, yes. Sovereign, also yes. Commercial operation is targeted for September 2026, pending AERB clearance. Two more 500 MWe units are sanctioned at Kalpakkam, with four more in the pipeline.

Why This Matters to Capital Allocators

1. Nuclear is the only scalable, low-carbon baseload

On a lifecycle basis, nuclear sits in the 10 to 15 gCO2 per kWh range, comparable to wind, well below solar at 40 to 50, and orders of magnitude below coal at over 800. Capacity factors above 90 percent. No diurnal curve. No seasonal dip. As data centres, AI training clusters and electrified industry push 24×7 load, the case for firm clean power gets harder to argue against, not easier.

2. The thorium endgame is real, even if it is decades out

If breeders mature, India’s thorium reserves could underwrite roughly 700 years of domestic generation, against about 200 years for its coal. Thorium also produces less long-lived waste and is meaningfully more proliferation-resistant than the plutonium cycle, since U-233 is far harder to weaponise. This is the moat. Not next quarter. Next century.

The SHANTI Act Just Opened a 60-Year Monopoly

For most of its history, India’s nuclear sector was a closed loop. The Atomic Energy Act of 1962 restricted ownership to state entities, mainly NPCIL and BHAVINI. Private players sold equipment and poured concrete. That was the ceiling.

The Sustainable Harnessing and Advancement of Nuclear Energy for Transforming India Act, 2025 (SHANTI) is a regime change. It repeals both the 1962 Atomic Energy Act and the 2010 Civil Liability for Nuclear Damage Act. Private companies, joint ventures and foreign players can now build, own, operate and decommission plants. Supplier liability has been rationalised, removing what was arguably the single largest deterrent for global OEMs. AERB gets statutory independence. The proposed Nuclear Energy Mission reforms include the creation of an Atomic Energy Regulatory Board and an Atomic Energy Disputes Tribunal. Sensitive functions, enrichment, reprocessing and heavy water, stay with the state. Everything else is fair game.

From state monopoly to market-enabled, in a single legislative move. This is the kind of structural shift that creates ten-year theses.

Who Is Already Moving

▪ Jindal Nuclear Power: USD 21 billion committed to 18 GWe over two decades, across PWRs, SMRs and Gen-IV designs.

▪ Tata Power: Signalled increasing interest in India’s emerging nuclear opportunity, including potential participation in the small modular reactor (SMR) ecosystem, as the sector opens to greater private-sector involvement.

▪ Vedanta: Expression of Interest for 5,000 MWe via global reactor vendor partnerships.

▪ Holtec International: Continues to expand its presence in India and has identified the country as a key market for the deployment of its SMR technology, reflecting growing industry confidence in India’s long-term nuclear roadmap.

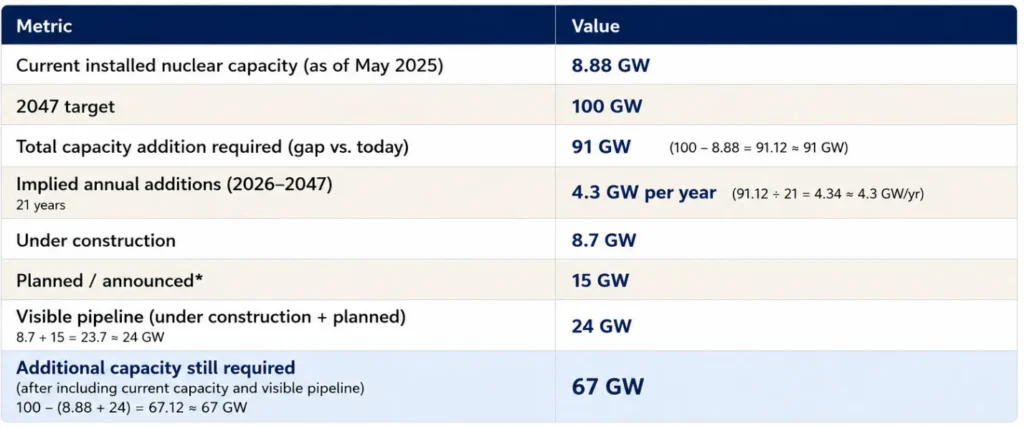

The Capacity Gap, in Numbers

Sources: PIB, ET, S&P, and World Nuclear Association

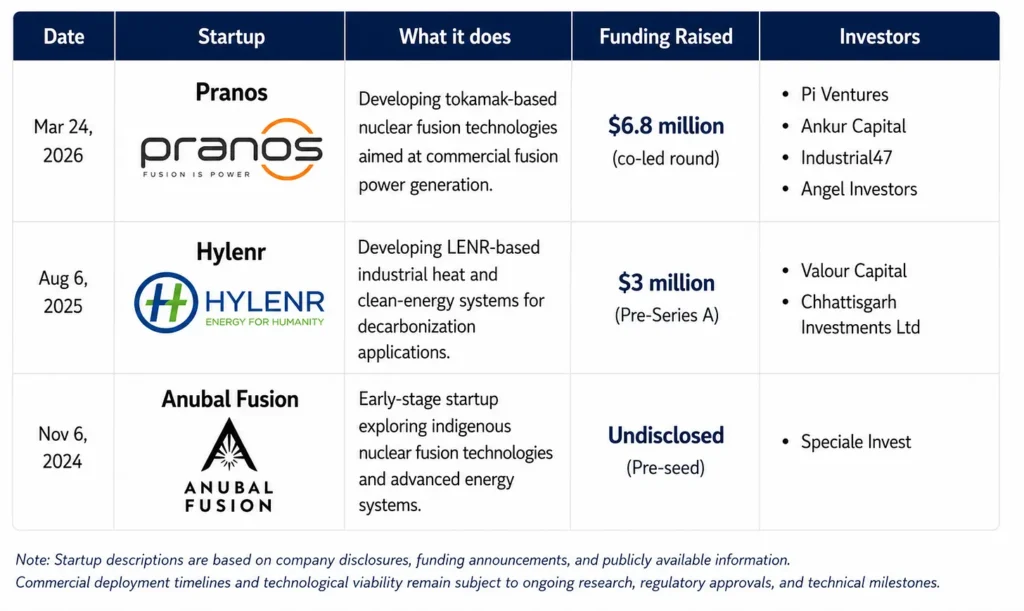

Startups in the space

While India’s nuclear sector has traditionally been dominated by public institutions, a new generation of startups is beginning to emerge across fusion, advanced reactor technologies, and next-generation nuclear fuels.

Sources: Tracxn, News articles

The Ostara Take

The 67 GW gap is the story. It cannot be closed with NPCIL alone. Closing it means private balance sheets, foreign OEMs, deep supply chains for forgings and pressure vessels, qualified fuel cycle services, advanced manufacturing for SMR components, and a domestic services layer for operations, maintenance and decommissioning. For early-stage investors, the interesting layer is everything around the reactor: digital twins for fuel handling, robotics for hot cells, materials science for high-temperature alloys, software for grid integration of variable plus firm portfolios, and human capital platforms for a workforce that has to scale roughly tenfold.

Nuclear has historically been a sector where policy moved in inches and capital arrived in trickles. SHANTI plus PFBR changes both vectors at once. The companies that read this correctly in 2026 will look obvious in 2036. The ones that wait for proof will be buying it at a different multiple.

Ostara in the News

1. Our Founder and CEO, Vasudha Madhavan authored a guest article in The Economic Times on 23 April 2026, exploring how India’s biofuel transition is creating a new class of “Urja Daatas” (energy providers) by placing farmers at the center of the clean energy ecosystem.Read the article here.

2. In an interview with AutoEV Times on 7 May 2026, Vasudha discussed the critical role of charging infrastructure in accelerating India’s EV transition.Read the interview here.

3. Vasudha was quoted in Business Standard on 27 May 2026, highlighting how AI is enabling a shift from reactive response to proactive, data-driven climate resilience planning.Read the article here.

4. Vasudha was featured in BW Businessworld on 15 May 2026, discussing how climate-related risks are becoming increasingly material for India’s financial sector.Read the article here.

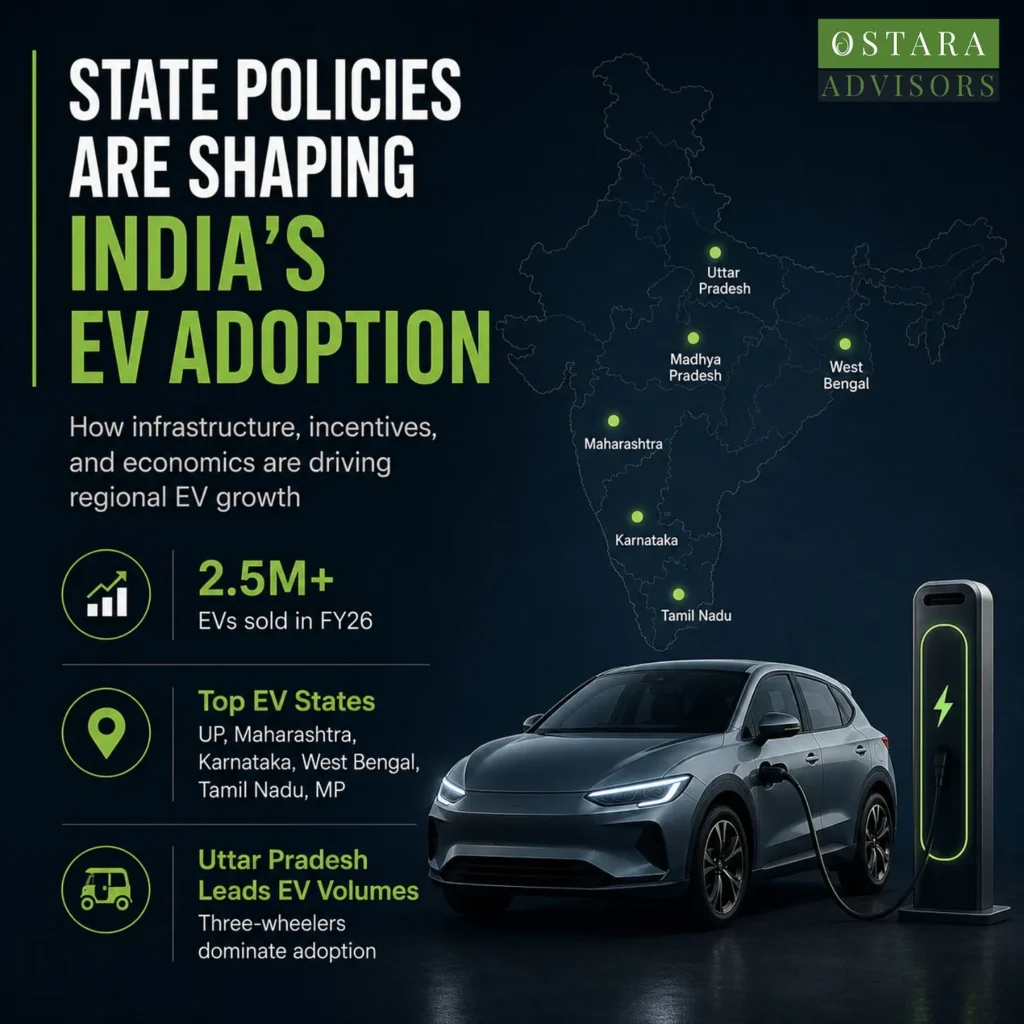

5. Vasudha was featured in The Economic Times on 3 May 2026, sharing insights on the evolving landscape of EV adoption across India. She noted that states are emerging as distinct EV markets with varying adoption patterns, driven by differences in policy frameworks, infrastructure readiness, affordability, and vehicle-use economics. Read the article here.