From the Founder’s desk

2025 – what a year it has been! We made magic with our conviction to transform mobility with climate capital and are now working on ever-more ambitious goals for India’s energy transition. As I look back on the year gone by, one thing is clear: climate tech in India has moved from momentum to maturity. Capital grew more discerning, founders more focused, and solutions more execution led.

As we step into the year ahead, I feel a sense of urgency and restlessness and also a quiet confidence: the foundations are in place, and the next phase will be defined by scale, substance, and staying power.

“We do not inherit the Earth from our ancestors; we borrow it from our children.”

– Native American proverb

2025 was a year of focused execution and steady expansion for Ostara Advisors. We announced the Routematic transaction, marking a key milestone in our mission to decarbonize traditional Corporate Mobility. Over the course of the year, we also deepened our work across Clean alternative Fuels, Circular Economy and expanded further into Energy and climate software, reflecting where capital and deployment are increasingly converging.

The year was equally defined by outreach and relationship-building. Our team travelled extensively across India and global markets, engaging with investors, strategics, and founders to advance conversations around India’s climate opportunity. Ostara’s work and perspectives have been featured multiple times across leading ecosystem platforms, including Entrepreneur India, ET Edge Insights, Asia Tech Daily, YourStory, and Inc42, reflecting its thought leadership and deep engagement with India’s climate-tech and startup ecosystem.

We also strengthened our leadership bench with the onboarding of Arjun Sondhi as Senior Vice President, reinforcing our commitment to building long-term capability as we scale our advisory work across climate and energy transition sectors.

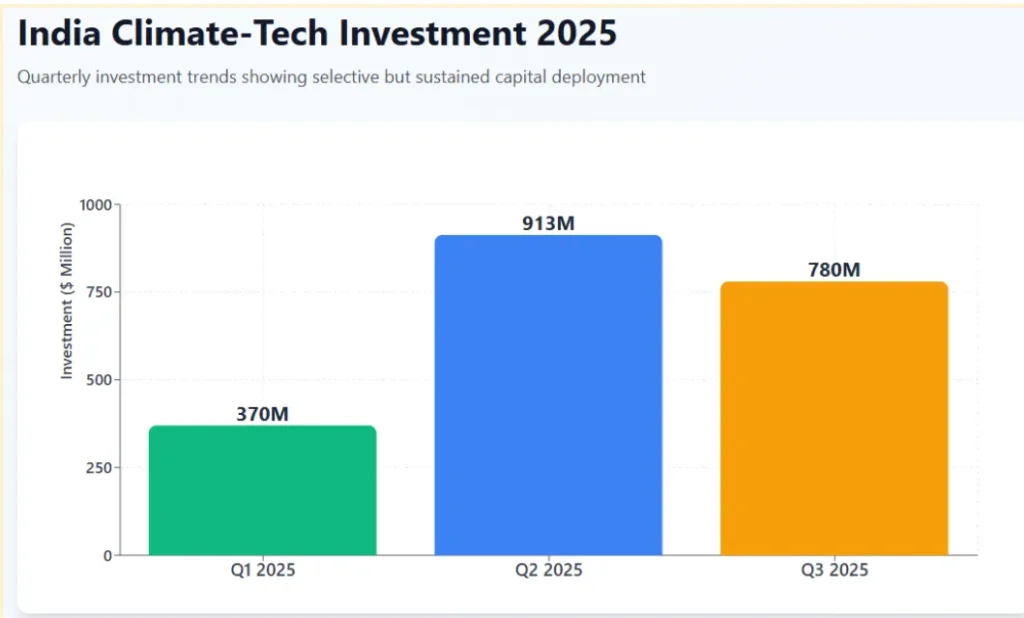

2025 Capital Flows: How Equity and Debt Unfolded Quarter by Quarter

Note: The analysis reflects updated data for the first three quarters of 2025. The quarterly figures capture total capital flows, including both equity and debt, and incorporate large infrastructure-linked transactions.

Source: The Climate Guys

India’s private climate-tech market entered 2025 on strong footing, with over $2 billion raised in the first nine months, implying 20–25% growth over the prior year. This momentum was built on 2024 deployments of ~$2.25 billion, led by Renewable Energy (50%) driven by utility-scale solar, wind, and manufacturing platforms, followed by Electric Mobility (27%), Energy Storage and Efficiency (10%), and early diversification into agritech, adaptation, and waste. In 2025, capital deployment remained selective rather than risk-off, with renewables still dominant and resilient early-to-growth PE activity in mobility and storage, pointing to disciplined capital backing scaled decarbonisation platforms rather than broad-based experimentation.

The Deals that got everyone talking: Major VC/PE Deals in 2025

1. Sun Mobility — $60M (Series B): July 2025Investors: Helios Climate and InfraCo Asia

Sector: Electric Mobility / Battery Swapping

Sun Mobility’s Series B funds the expansion of its battery-swapping infrastructure across India and select international markets. Investors are backing platform-led EV infrastructure that lowers adoption barriers in high-utilisation mobility segments.

2. Jupiter International — $58.2M (Private Equity): April 2025Investors: ValueQuest and affiliates

Sector: Renewable Energy / Solar Manufacturing

The capital raise is aimed at scaling solar cell and module manufacturing capacity. The deal underscores investor confidence in execution-driven manufacturing platforms aligned with India’s PLI incentives and import substitution strategy.

3. Routematic — $40M (Series C): May 2025Investors: Fullerton Fund Management, Shift4Good

Sector: Electric Mobility / Enterprise Transport

Routematic’s Series C supports expansion of AI-optimised and EV-enabled employee transport across major Indian cities. Investors are backing asset-light, tech-led mobility platforms with predictable enterprise revenues and measurable emissions impact.

4. Varaha — $30 M (Series B): November 2025Investors: Mirova

Sector: Regenerative Farming

Mirova invested in Indian climate-tech startup Varaha through a structured carbon-financing arrangement rather than a traditional equity round, marking its first carbon investment in India. The capital will be used to scale Varaha’s regenerative agriculture programme across northern India, expanding its Kheti project in Haryana and Punjab, which already covers over 200,000 hectares and is expected to reach around 337,000 farmers across 675,000 hectares.

5. Aerem — $11.7M (Series A): April 2025

Investors: University of Tokyo Edge Capital Partners (UTEC), British International Investment (BII), SE Ventures, Riverwalk Holdings, Blume Ventures, and Avaana Capital

Sector: Distributed Solar / Climate Fintech

Aerem’s Series A supports scaling of its rooftop solar platform combining financing, EPC marketplace, and digital execution. Investors are backing full-stack models that simplify solar adoption for MSMEs.

The Year that Climate Graduated: IPOs that defined 2025

Ather Energy: April 2025

Ather Energy was the marquee climate-tech IPO of 2025, raising ~$352 million as a scaled electric two-wheeler OEM with strong brand recall, in-house R&D, and an integrated fast-charging network. The listing marked its transition to public-market scale, with proceeds funding a new Maharashtra manufacturing facility, product and software development, charging expansion, and partial debt repayment.

Vikram Solar: August 2025

Vikram Solar raised about $236 million through its IPO, emerging as a public-market play on India’s solar manufacturing expansion. As an integrated supplier to utility-scale and rooftop projects in India and overseas, the company went public to fund backward integration and capacity growth. Proceeds were directed toward scaling cell and module manufacturing, investing in advanced PV technologies, and strengthening the balance sheet.

TruAlt Bioenergy raised around $95 million through its IPO, marking a significant capital raise in India’s renewable fuels segment. The company, a leading producer of ethanol and biofuels with substantial installed capacity, priced its shares in the upper band and listed with a premium, reflecting strong investor interest in sustainable energy solutions. Proceeds from the IPO are being used to support working capital and fund expansion, including new ethanol production facilities, positioning TruAlt to scale in line with India’s growing emphasis on cleaner fuels.

Catalyst of Change: The Policies that impacted 2025

In 2025, India’s policy framework emerged as a key driver of climate capital, underpinned by stability and execution certainty. Production Linked Incentive (PLI) schemes materially improved project economics and accelerated domestic manufacturing across solar, batteries, EV components, and energy storage, while public-sector offtake through SECI, NTPC, and state DISCOMs significantly reduced revenue risk. In biofuels, the SATAT programme enabled long-term CBG offtake, supported by a clear 20% ethanol blending target and emerging CBG blending mandates. Together, these measures translated policy intent into investable, bankable projects, attracting global climate capital toward scaled infrastructure and manufacturing platforms rather than early-stage experimentation.

Emerging Climate Investment Themes Heading into 2026

As India enters 2026, climate capital is shifting decisively from pilots to platforms – backing sectors with policy tailwinds, execution depth, and scale-ready economics.

Energy Storage & Clean Manufacturing are emerging as core infrastructure plays, with capital favouring integrated platforms that link battery manufacturing to downstream deployment.

Electric Mobility Infrastructure is gaining momentum beyond OEMs, as charging and battery-swapping networks attract asset-backed, enterprise-led capital.

Climate Data & Software is becoming indispensable, driven by emissions reporting, energy efficiency mandates, and the digitisation of physical climate assets.

Biofuels & Waste-to-Energy, especially CBG under SATAT, stand out as one of the most bankable, policy-backed decarbonisation themes.

Adaptation & Resource Efficiency – water, cooling, and climate-resilient agriculture – remain underpenetrated but are poised to move from pilots to early scale as climate stress intensifies.

The signal for 2026: Capital is rewarding readiness – where policy, demand, and execution converge.