We started covering Freight Electrification in our newsletterlast month, as we believe this to be one of the most compelling use-cases for the clean mobility transition. We wrote about various zero-emission technologies currently available for freight vehicles, the limitations of these technologies for long-haul trucking and also shared a snapshot of the Indian policy framework for electric freight and logistics.

Quite coincidentally, earlier this month, we were invited by NITI Aayog, the premier policy ‘Think tank’ of the Government of India to the launch of e-FAST India (Electric Freight Accelerator for Sustainable Transport – India), the country’s first national electric freight platform. This platform, launched in collaboration with WRI India and the World Economic Forum (WEF), aims to bring together Shippers, Truckers, Fleet Aggregators, OEMs, EV Financiers and other stakeholders to accelerate the decarbonisation of India’s freight and logistics sector. The platform also saw the release of the RMI report on Pathways to Zero-Emission Truck Deployment in India.

This marks a significant positive move towards Freight Electrification in India and we could not be prouder to have participated.

Moving on to our this month’s edition of the Ostara Newsletter.

In our previous edition, we delved into the budding freight electrification trend in India. This month, let’s have a look at how the world is electrifying freight and some interesting case studies from across the globe.

Rising gasoline, fuel, diesel, and petrol prices are offering attractive chances for the global electric truck market to take off. Furthermore, prominent market participants are utilising renewable energy sources in the production of electric vehicles on a global scale. Countries and states worldwide are setting zero-emissions freight targets, and there are now multilateral actions aimed at accelerating the manufacturing of Zero-emission Trucks (ZETs).

In the electric truck sector, the concept of solar-powered trucks and recharge stations is gaining traction, with many countries increasingly forming partnerships to develop joint pathways to reduce vehicle emissions, particularly for scaling electric Heavy-Duty Trucks (HDTs).

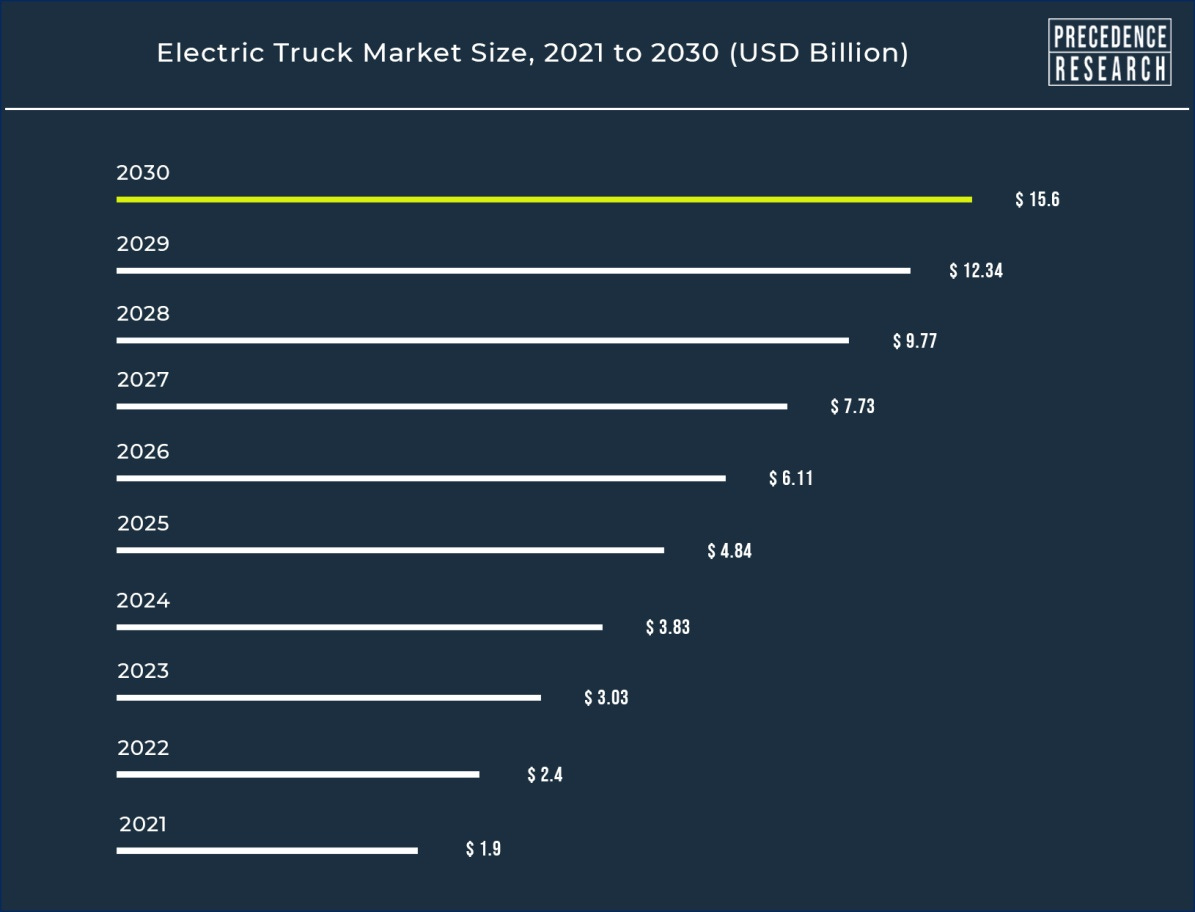

The Global electric trucks market is projected to reach 1,413,694 units by 2030, at a CAGR of 39.7% from 2021 to 2030.

Additionally, as part of the Drive-to-Zero Campaign, several European countries as well as Canada and Australia signed a memorandum of understanding to foster leadership and international coordination to accelerate ZET adoption.

The Frontrunner in Freight Electrification: Shenzhen

The city of Shenzhen, in southeastern China, is the global pioneer of electric logistics vehicles (ELVs). Shenzhen began to implement a policy framework to support ELVs in 2015, increasing the share of ELVs from less than 1% to over 30% . This is due in part to the near-ubiquitous charging infrastructure that has been installed across the region.

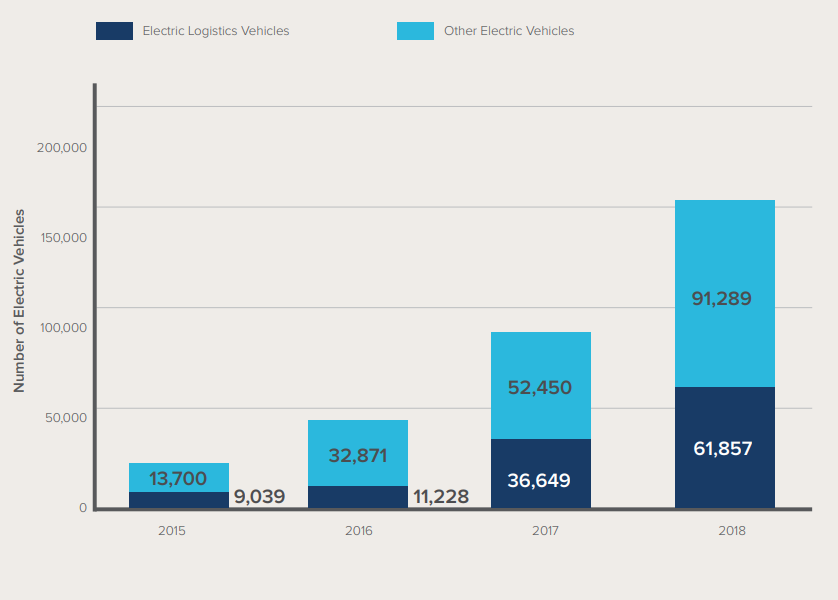

From the beginning of 2015 to the end of 2018, Shenzhen’s fleet of electric logistics vehicles, vans, and light/medium trucks expanded from 300 to approximately 61,857.

Shenzhen EV Population (2015-18)– Diandong Alliance

As of 2019, the ELV population stands at 70,417, with more than 80% of the ELVs being registered during or after 2017. The ELV fleet is composed of 39,363 minivans, 24,330 light trucks, and 5,597 medium vans.

While vigorously promoting the use of ELVs, Shenzhen is also actively building out the infrastructure to meet the demand for charging from this rapidly expanding vehicle fleet. By the end of 2019, about 83,000 public chargers had been built in the city—including about 30,000 DC fast chargers.

World’s Largest EV Fast Charging Station, Shenzhen

On the commercial side two key factors have supported the rapid growth of the vehicle market:

Strong model availability, with over 45 brands delivering electric urban vehicles at acceptable price points and operational performance

The emergence of leasing companies that bundle the provision of vehicles, charging, maintenance, and, at times, even drivers for a flat monthly or annual fee

Policy support has been a key driver of ELV adoption in Shenzhen. In the Shenzhen market, policymakers have implemented four types of policy to spur rapid adoption of ELVs and associated charging infrastructure:

Subsidies lower the upfront cost of ELVs compared with similar ICE vehicle alternatives and support private deployment of charging infrastructure.

Preferential road access for ELVs increases their utilisation and, therefore, revenue.

Preferential electricity rates and fee exemptions for charging operators, and therefore ELV operators, lower fuel costs.

Mandates and targets at the city and district level for the number of chargers within a specified timeline support growth of the charging network.

Ownership Models

Another notable feature of the ELV market in Shenzhen is the prevalence of leasing rather than vehicle ownership, which is how more than 95% of ELVs are acquired by operators. Short-term leasing models, with contracts as short as one month, have been critical for enabling operators to adopt ELVs with confidence.

There are three major reasons that operators choose to lease, rather than to purchase, ELV:

Lack of a strong ecosystem of maintenance and refuelling for ELVs: Individual vehicle operators cannot build up maintenance and charging systems themselves, but leasing companies, which own thousands of vehicles, can. Once leasing companies establish these systems, they can provide them to customers as an overall package when leasing the vehicle.

Cost structure of vehicles: Vehicle operators often have little or no access to credit. However, leasing companies often have strong balance sheets and are able to finance the high up-front cost of vehicles at relatively low rates.

In Europe, heavy vehicles account for 5-6% of total CO2 emissions. Policymakers have been contemplating ways to reduce these amounts. Among the many initiatives, electrification is one that’s fast gaining traction.

The electrification scenario in Europe is very optimistic, with zero-emission transport gaining momentum in the continent. Other than vehicle OEMs making strides on the R&D front, the governments are making moves to further the transition to EVs:

MOVE21 and FREVUE are initiatives funded by the EU to encourage, and promote, electrification of freight vehicles.

Switzerland is encouraging fuel cell electric truck growth through its road tax on diesel truck operations, making alternative fuels more attractive for large Swiss retail associations.

In February 2022, EU member states have adopted new legislation which states that all EU member states have until 2023 to implement a new system of road tolls that give big incentives for zero-emissions trucks.

By May 2023, haulers operating zero-emissions trucks, i.e., battery electric or hydrogen, must be given at least 50% discounts on distance-based road tolls. Member states could opt to levy extra CO2-based charges on fossil fuel lorries instead or implement both measures. With road tolls costing haulers up to EUR 25,000 a year per truck annually, switching to zero-emissions vehicles will cut their overheads considerably.

From the market standpoint, the Europe Electric Truck Market was valued at USD 286.87 million in 2021 and is expected to reach USD 4,358.25 million in 2027 by registering a CAGR of 57.13% during the forecast period (2022 – 2027)with medium- and heavy-duty trucks accounting for close to 70% of road transport emissions.

On June 25, 2020, the California Air Resources Board (CARB) unanimously adopted the world’s first zero-emission commercial truck requirement, the Advanced Clean Trucks rule.

The regulation, first of its kind in the world to require manufacturers to sell increasing percentages of zero-emission trucks, is expected to reduce the life cycle emission of greenhouse gases (GHGs), eliminate tailpipe emissions of air pollutants, and foster a market for zero-emission Heavy-Duty Trucks(HDTs).

Since California holds a sizable share of the HDT market in the United States, this regulation will have implications far beyond the state’s borders. The truck brands that represent the majority of sales in California sell in multiple regions around the world.

The sales requirements in the ACT are complemented by a series of fleet purchase requirements, such as the Innovative Clean Transit rule for buses, which goes into effect in 2023 and requires 100% zero-emission bus purchases by 2029.

At the invitation of Impact Investors Council, we also penned down our views on the private capital flows into the Indian EV ecosystem in their inaugural India Climate Bulletin released at their Flagship Impact Investor Conference, Prabhav 2022, in New Delhi.

Ostara Advisors was invited to share their views at WRI India’s workshop on financing and creating an investment ecosystem for #ElectricRickshaws in India. The workshop saw industry stakeholders discuss current challenges and suggest ways to optimise innovative financial tools to accelerate the e-rickshaw transition.

Mukund is a seasoned investment banker with 27 years of experience in advising companies on M&A and capital raising transactions. He has served most recently as Joint Managing Director at Motilal Oswal Investment Banking, where he worked from June 2014 to January 2021. During his career, he has facilitated over 70 strategic financial transactions including Motherson Sumi’s acquisition of PKC Group (Finland), sale of Aurangabad Electricals to Mahindra CIE, Siemens’ sale of Bangalore Airport, sale of Spicejet, Aegis’ acquisition of PeopleSupport (USA), sale of Air Deccan among others. Mukund has extensive experience in raising private equity funding as well as in the capital markets including IPOs, follow-on offerings, GDRs and ADRs for L&T Finance, Indostar, Dixon Technologies, Bharat Financial Inclusion, Tata Consultancy Services (TCS), Wipro, GAIL, etc.

Mukund has earlier worked for 9 years at Edelweiss Financial Services and started his career in 1996 with a 9-year stint at Morgan Stanley. Mr. Ranganathan holds a B.Tech degree in Electrical Engineering from Indian Institute of Technology Madras (1994) and a PGDM from Indian Institute of Management, Ahmedabad (1996).

A pioneer in India’s electric mobility and climate-tech investment ecosystem, Vasudha is the Founder & CEO of Ostara Advisors and has led transformational deals, including India’s first M&A in the electric two-wheeler sector. With over 22 years of experience in Corporate & Investment Banking, she has catalyzed global capital flows into clean mobility, making Ostara Advisors a leader in growth-stage fundraising and M&A.

She has previously worked at Citibank, where she was responsible for setting up & expanding Citi’s India’s ‘Private Equity and Hedge Fund’ coverage vertical, ICICI Bank’s Treasury Division & the Product Technology Group and boutique investment banking firms and made her debut in the Top 20 on the All-India M&A League Tables in late-2018. In 2023, Vasudha was felicitated by India Energy Storage Alliance (IESA) as one of the Top 40 ‘Women leaders driving Energy sector in India’.

After an illustrious career in the Banking sector where she was known for her business acumen as well as her intrapreneur skills, she honed in on Climate-Tech as the vertical she wanted to make a mark in. Vasudha founded Ostara Advisors in 2015 to catalyze global capital flows into the clean mobility and climate-tech ecosystem in India. Taking a thought-leadership approach in these sectors, the firm is today an early mover in institutionalizing fund-raising in these sectors with a focus on growth stage fund-raising and M&A transactions.

Vasudha is also a mentor at Aspire for Her, a unique organisation that enables women to join and stay in the workforce, through campus engagement, mentorships and skilling workshops. Their vision is to impact 1 million+ women and add $5B to India’s GDP through increased participation of women in the workforce by 2025.

Vasudha earned her MBA in Finance from XLRI, Jamshedpur, India and her Bachelor’s degree in Commerce from Mount Carmel College, Bangalore, India. She is also a certified Advanced Scuba Diver and enjoys photography, having held several solo and group exhibitions of her work.

R. 'Shanx' Ravisankar

Industry Expert – Financial Technology and Cloud Solutions

Shanx is a founding member and former CEO of Oracle Financial Services Software, (formerly known as i-flex Solutions, the company was acquired by Oracle in 2006). Shanx retired in 2011 as the Chief Operating Officer, Oracle Financial Services Global Business Unit (FSGBU). As a technology leader, he has also been profiled in leading trade and industry publications. In 2008, Shanx was selected as one of the 50 Outstanding Asian American business leaders. This accolade celebrates Asian business leaders and recognizes their pivotal roles in Corporate America. Shanx is an engineering graduate from the Indian Institute of Technology, Chennai, and has an MBA in Management from the Indian Institute of Management, Ahmedabad, India.

Get our monthly exclusive updates on the Electric Mobility ecosystem